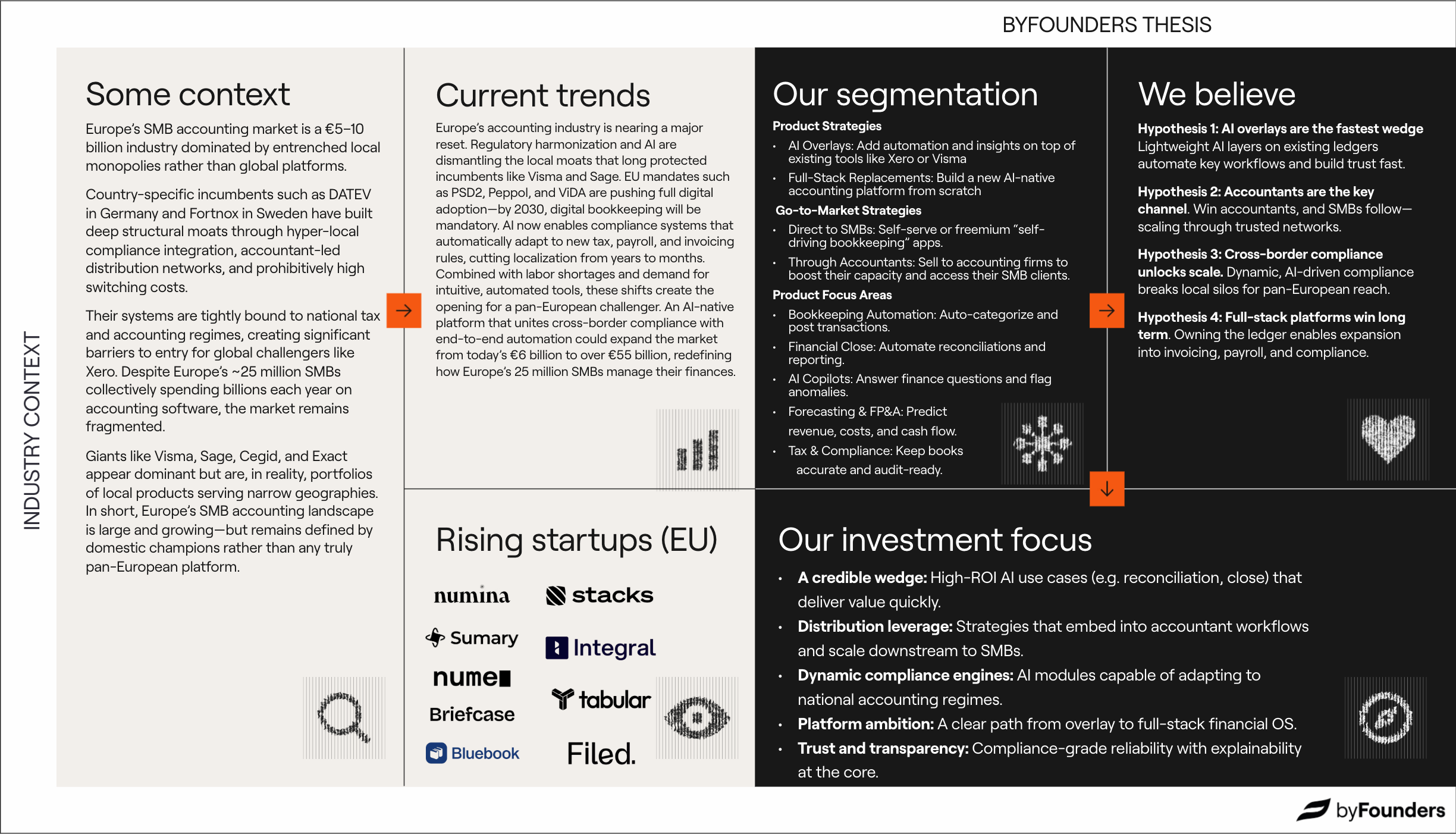

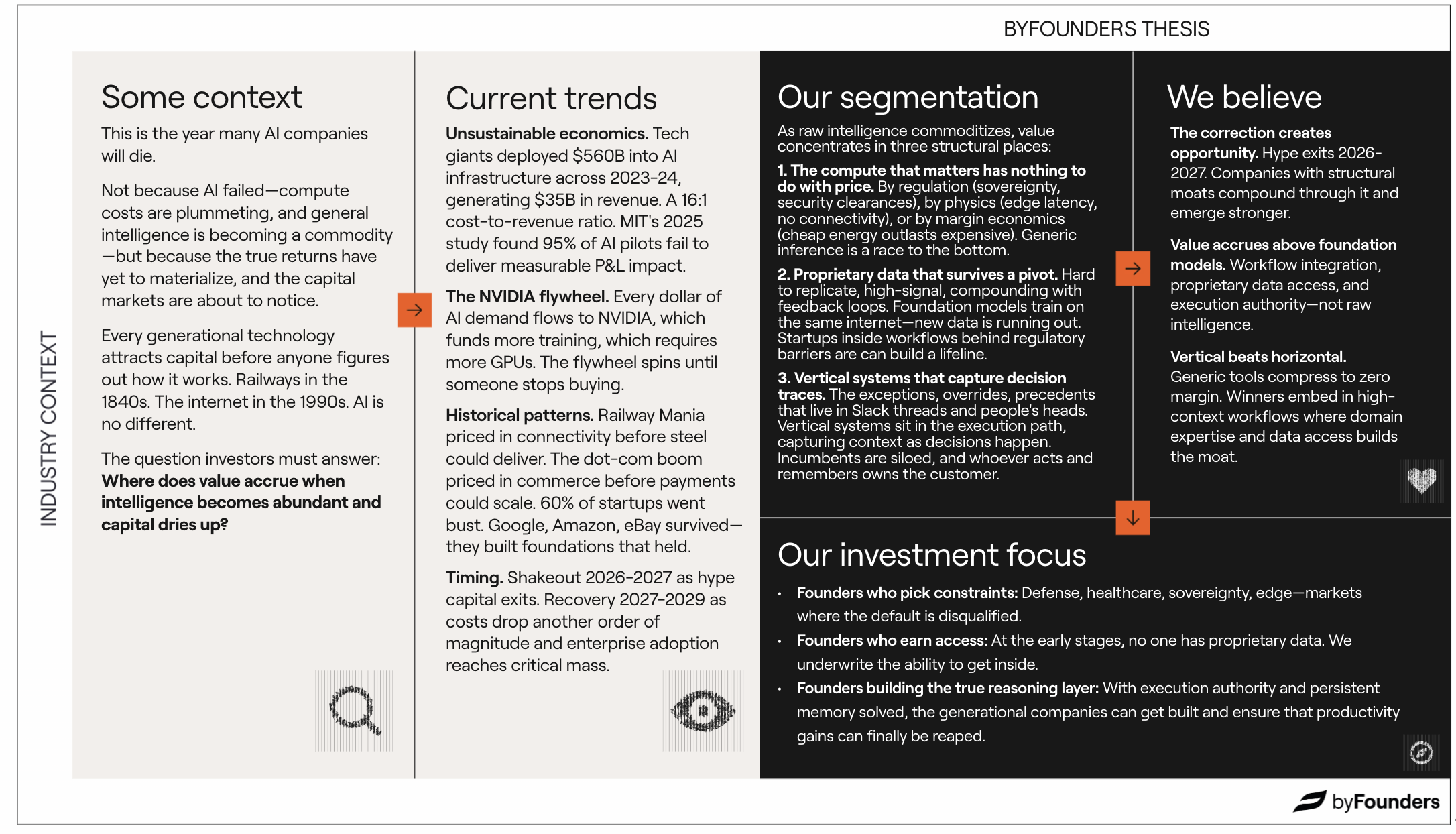

European Accounting: A House of Cards About to Fall

A €55B opportunity is emerging as AI and regulatory convergence erode local moats and unlock cross-border scale.

.png)

Europe’s SMB Accounting Market: Fractured and Dominated by Local Monopolies

Entrenched Local Incumbents

SMB accounting in Europe is shaped by country-specific incumbents that hold near-monopolies in their domestic markets. Over decades, these firms have embedded themselves into national infrastructure by encoding local GAAP standards, payroll formats, and tax schemas directly into their products, while distributing primarily through accountant networks. The result is a €5–10 billion market that is large in aggregate, but fractured into local monopolies.

Why Local Monopolies Persist

Three structural moats explain the resilience of incumbents:

Hyper-local compliance barriers. Every country maintains its own accounting regime (VAT, GAAP, e-filing formats etc.) and incumbents have built systems tightly coupled to those rules. DATEV in Germany, for instance, updates automatically as tax law changes. Global challengers like Xero struggle in such markets because their software simply doesn’t comply.

Accountant-driven network effects. In most European countries, accountants remain the primary distribution channel. Once a platform gains traction with firms, their SMB clients follow, locking in both sides of the market. For challengers, breaking in requires enterprise-style sales into accounting practices or circumventing them altogether with self-serve tools.

**High switching costs.**Years of financial history, audit trails, and compliance data are embedded in legacy systems. Migration is complex and risky, and incumbents often make exporting data deliberately difficult. For most SMBs, the cost and risk of switching outweigh the benefits of a new system.

Market size is large…

Europe has roughly 25 million SMBs who spend between €200 and €2,000 per year on software or accounting services. Around half of these firms outsource their bookkeeping. Today, SMB accounting software already represents a ~€6 billion market, projected to grow at 8% CAGR to €8.6 billion by 2030.

…but extremely fragmented

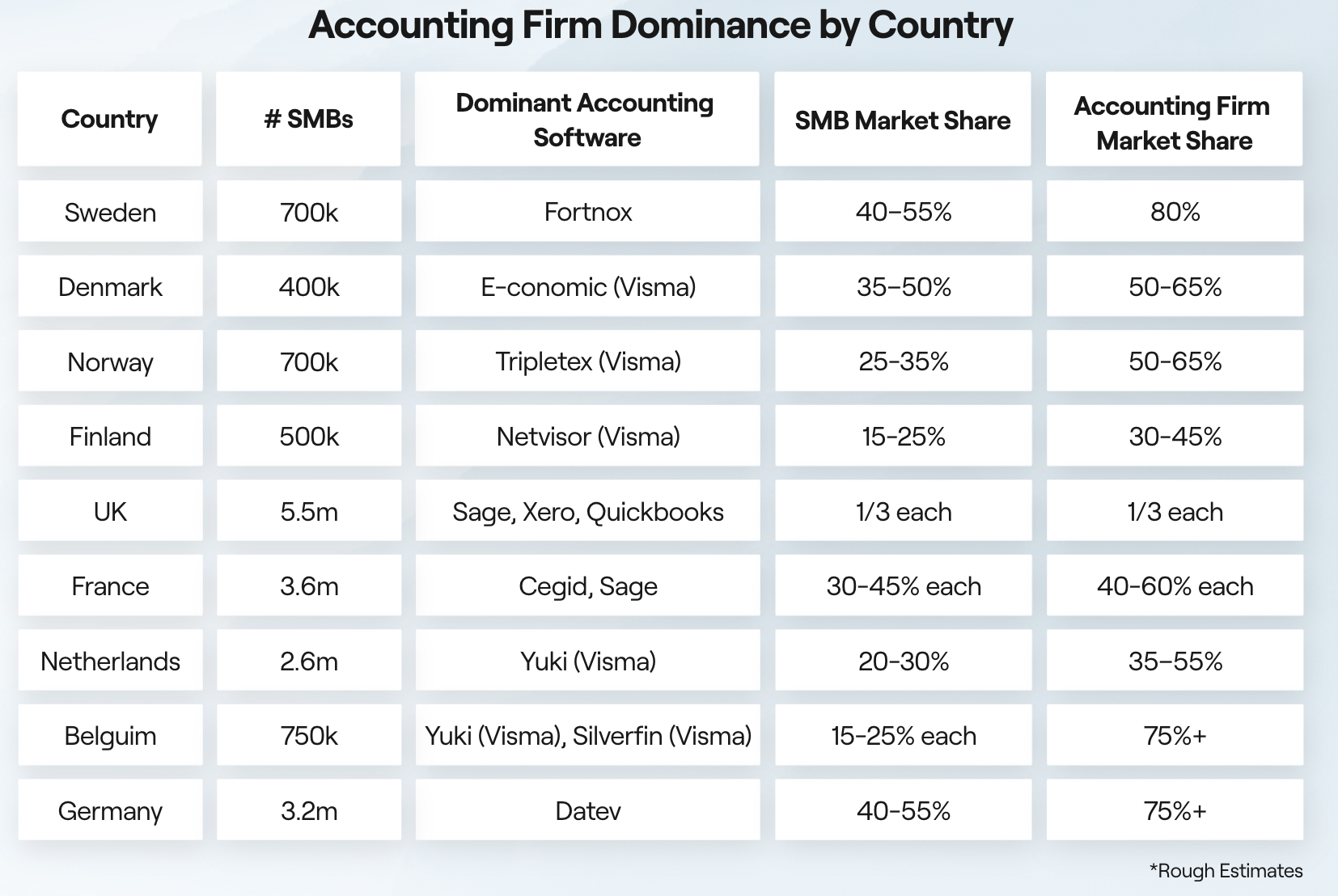

Despite the size of the opportunity, the market remains fragmented. Visma is valued at €19–22 billion and built through more than 190 acquisitions, one of its largest products, Denmark’s e-conomic, serves only ~180–200,000 SMBs. The rest of its portfolio consists of small, country-specific brands. Sage presents a similar story. With a $14 billion market cap and ~38 acquisitions, it appears a global leader but is in reality a portfolio of regional products. Across the continent the pattern repeats. Cegid in France and Iberia (€6.8B after merging with Grupo Primavera) remains a patchwork of local solutions. Fortnox dominates Sweden but, despite a ~$5.5 billion take-private bid, generates only ~$200 million in annual revenue. Exact, acquired by KKR for €1.5 billion, serves ~400,000 SMBs but is largely confined to the Benelux region. Germany’s DATEV, structured as a cooperative, counts over 800,000 customers yet operates almost exclusively at home.

In short: incumbents are large in aggregate but fragmented in practice. Europe’s SMB accounting market is still defined by roll-ups, national champions, and domestic monopolies. No one has yet built a truly pan-European platform.

.png)

A new entrant will capture this market. The only question is: who?

Europe is moving toward a harmonized regulatory environment. Accounting, tax, and reporting standards that were once country-specific are being standardized, lowering the barriers for software that can operate across borders. Advances in LLMs, amplify this shift by making it easier to adapt to new compliance requirements.

- Regulatory tailwinds. EU initiatives such as PSD2 (payments), Peppol (e-invoicing), and ViDA (VAT in the Digital Age), alongside national e-invoicing mandates, are accelerating digital adoption. By 2030, digital bookkeeping will essentially be mandatory across the EU.

- The AI unlock. Rather than coding each national standard line by line, AI can ingest VAT schemas, payroll rules, and tax forms directly—allowing faster, more dynamic localization.

- Incumbent weakness. Incumbents like Visma and Sage rely on fragmented, country-specific monopolies. A unified cross-border product would cannibalize their portfolios, leaving little incentive for them to lead change.

Together, these forces create the conditions for a pan-European challenger.

AI’s potential to reshape incumbent moats

AI could erode the structural advantages incumbents enjoy today by making compliance and workflows both dynamic and scalable.

- AI-native compliance automation. Government e-invoicing schemas, VAT updates, or payroll standards could be ingested and adapted automatically, compressing localization cycles from years to months.

- Improved UX and workflow automation. Many incumbent tools remain form-heavy and dated. AI-native products can offer a different model: conversational interfaces allowing users to query their accounts in plain language, automatic reconciliations, proactive alerts, and near-zero manual data entry.

- Labor shortages as a forcing function. The accounting profession faces a shrinking pipeline of talent, with 75% of US CPAs set to retire in the next 15 years and similar dynamics in Europe. AI can act as a “digital junior accountant,” handling categorization, reconciliations, and basic reporting. This structural shortage creates pressure for adoption, even among conservative firms.

The result is a clear opening. AI is not an incremental feature but a force that could undercut incumbents’ national moats and redefine how accounting software is built and delivered in Europe.

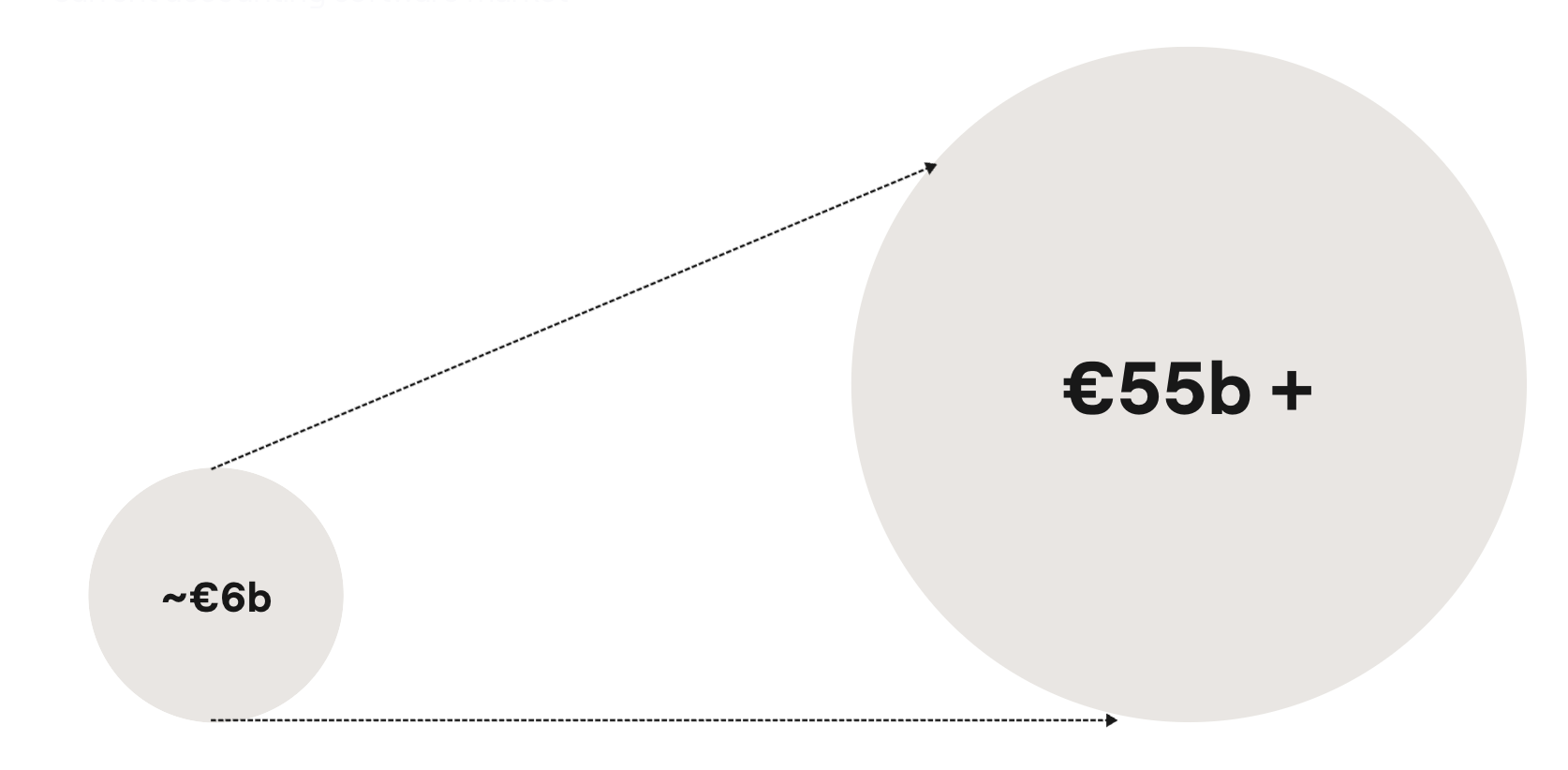

Allowing the Market to Expand 10x

If AI-native platforms can combine cross-border compliance with AI automation, the addressable market is no longer just today’s software spend. It extends into the far larger pools of spend currently flowing to external accountants and internal bookkeepers.

- External accountant spend (~€21B). Europe’s 25 million SMBs, with around 60% outsourcing bookkeeping, spend on average €1,400 annually per firm. This alone represents a €21 billion pool of spend.

- Internal accountant spend (~€27.5B). Many SMBs employ partial or full-time bookkeepers. Assuming 0.25 FTE per SMB at an average salary of €22,000, and applying a conservative 20% AI substitution rate, this translates into €27.5 billion of addressable value.

Together, these figures suggest that the market for AI-native accounting could expand to more than €55 billion—an order of magnitude larger than today’s €6 billion software market.

This opens two disruptive product paths

The expansion of the market creates two distinct product strategies for challengers. The choice depends on positioning relative to incumbents such as Fortnox, Visma/e-conomic, Sage, Xero, and QuickBooks: whether to build on top of existing platforms or seek to replace them outright.

AI overlays.

These products integrate directly with incumbent ledgers, adding intelligence and automation without requiring a platform switch. By abstracting over existing systems, overlays can act as AI co-pilots — delivering reconciliations, insights, and workflow automation on top of legacy software. The benefit is low switching friction: SMBs and their accountants can adopt AI enhancements without disrupting core processes.

Full-stack replacements (own the ledger).

This strategy rebuilds the ledger from scratch, embedding AI at the core. The goal is a unified, cross-border accounting platform that controls the entire user experience. It is more ambitious but also more demanding: challengers must replicate years of incumbent product development from invoicing to tax modules while simultaneously proving that an AI-native experience delivers enough value to justify migration.

…with Two Go-to-Market Paths

Accounting software is inherently a two-sided platform. Products must reach both SMBs and the accountants who serve them. This creates two primary go-to-market strategies:

Sell directly to SMBs via self-serve products.

Often via a freemium or product-led model, designed to gain adoption quickly. The pitch: a “self-driving” bookkeeping app that business owners can use directly without relying on external accountants.

Target accountants to 10× their capacity and win downstream clients.

By selling to accounting and CPA firms, products can automate workflows and enable firms to serve many more SMB clients with the same staff. This taps into existing trust relationships and entrenched distribution. Since most SMBs still rely on accountants, winning the accountant often means winning their client base.

.png)

Core Product Focus Areas

AI startups in accounting typically focus on a handful of recurring pain points across the finance function. The first is bookkeeping automation — removing the manual work of categorisation and data entry by auto-classifying bank feed transactions, bills, and receipts directly into the ledger. Closely linked is the financial close, where products aim to shorten reconciliation cycles and automate the preparation of month-end financial statements, targeting one of the most time-consuming parts of accounting.

A third area is the rise of AI copilots and workflows. These tools embed assistants directly into the finance stack: some act as conversational copilots that answer natural-language questions like “Why is our gross margin down this month?” with supporting figures, while others operate as agentic systems that prepare draft tax returns, monitor books continuously for anomalies, and escalate only when human input is required.

Startups are also extending into forecasting, budgeting, and FP&A. By using historical data and machine learning, they generate projections for revenue, expenses, and cash flow — capabilities once restricted to larger finance teams. Finally, there is tax and compliance, where AI is applied to ensure books are audit-ready, cross-checking transactions against contracts and surfacing potential discrepancies before they become issues.

byFounders Thesis: AI-Native Accounting Platform for European SMBs

At byFounders, we believe Europe’s fragmented accounting landscape is at an inflection point. Local incumbents have entrenched themselves in national markets for decades, but regulatory convergence and AI are lowering the barriers to scale. The company that combines automation, compliance, and distribution has the potential to become the trusted financial OS for 25M+ SMBs.

Hypothesis 1: AI overlays are the fastest wedge

The quickest path to adoption is through low-friction AI layers that sit on top of existing ledgers (e.g. e-conomic, Xero, QuickBooks). Automating reconciliation, close, and forecasting creates immediate ROI without forcing platform migration, building trust and usage early.

Hypothesis 2: Accountants remain the key distribution channel

Accounting software is inherently two-sided. SMBs use the tools their accountants adopt. By enabling firms to 10× client capacity, challengers can scale through existing trust relationships and tap into downstream adoption, a far more efficient route than selling directly to SMBs alone.

Hypothesis 3: Cross-border compliance is the unlock for scale

Incumbents thrive on local moats, hard-coded around tax, GAAP, and payroll rules. AI-native compliance engines that ingest regulatory changes dynamically can break this barrier. This capability is essential to escape local ceilings and build a truly pan-European platform.

Hypothesis 4: Full-stack platforms capture long-term value

Overlays are the entry point, but the endgame is to own the ledger. Expanding into invoicing, payroll, and compliance increases ARPU, product defensibility, and user control. The companies that move from AI copilot to Financial OS will define the market.

byFounders Investment Focus

Our focus is on ambitious teams who can navigate regulation, design trustworthy AI products, and execute on multi-stage roadmaps. We look for:

- A credible wedge: High-ROI AI use cases (e.g. reconciliation, close) that deliver value quickly.

- Distribution leverage: Strategies that embed into accountant workflows and scale downstream to SMBs.

- Dynamic compliance engines: AI modules capable of adapting to national accounting regimes.

- Platform ambition: A clear path from overlay to full-stack financial OS.

- Trust and transparency: Compliance-grade reliability with explainability at the core.

Related

Sign up to our newsletter.

Follow us