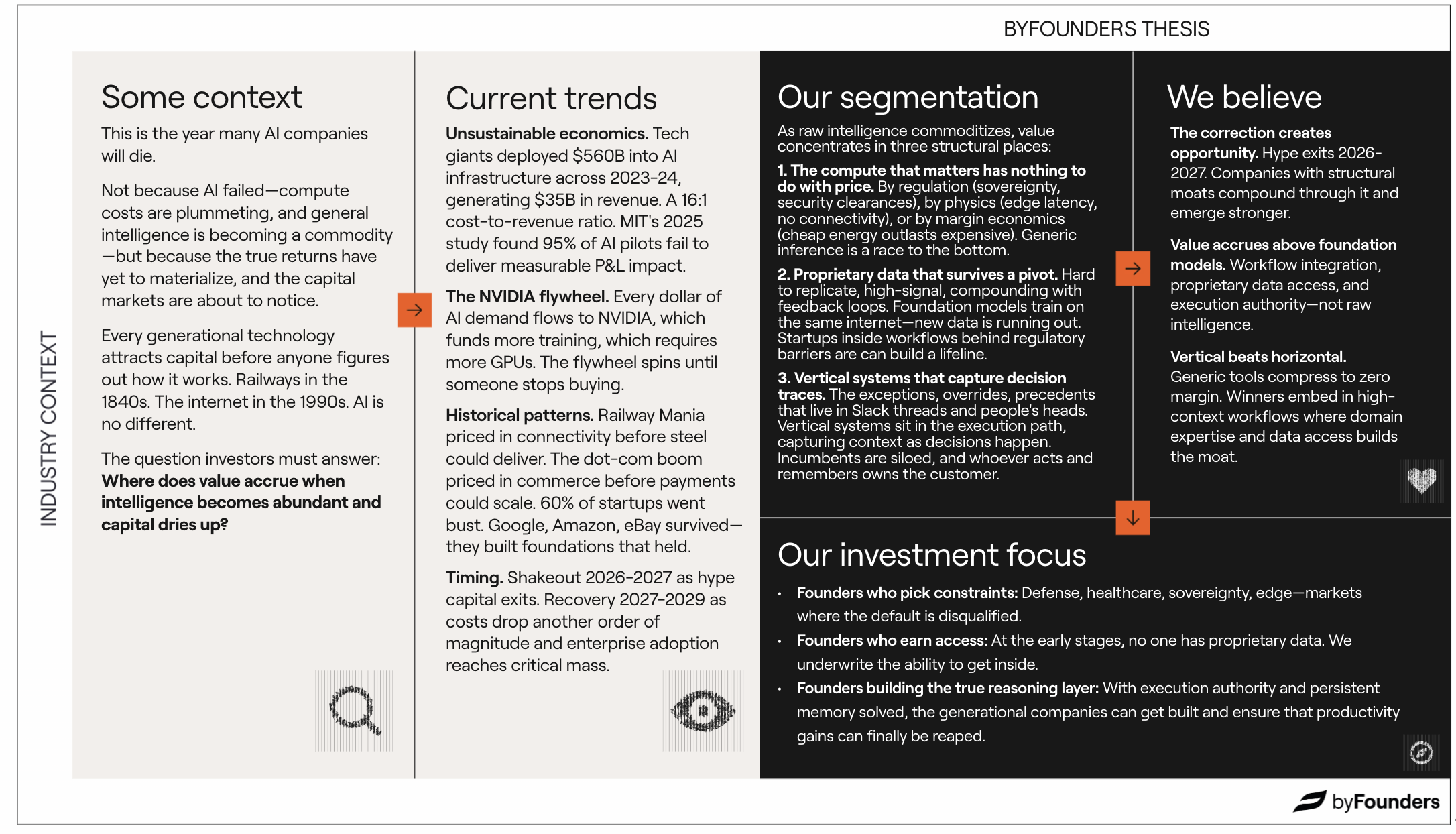

Clean Baseload Energy: Reality or Moonshot?

As electricity demand soars and renewables fall short on reliability, clean baseload power—like geothermal, advanced fission, and fusion—emerges as a crucial, investable solution for a stable, net-zero energy future.

Clean Baseload Energy: Reality or Moonshot?

I’ve already written about why energy markets are electric — and the opportunities that emerge as renewables take centre stage in our power mix.

But the bigger opportunity might lie in what happens when the sun doesn’t shine and the wind doesn’t blow.

Electricity demand is surging — fuelled by AI compute, increased cooling needs, industrial growth, electric vehicle adoption, our ongoing ambition to electrify everything, the list goes on. And while wind and solar are critical to decarbonizing the grid, they can’t carry the load alone.

Even though we added more solar to the grid in 2024 than any year in history, it still wasn’t enough. Global energy demand grew so rapidly that we had no choice but to fill the gap with fossil fuels.

As the IEA put it: "The expanding supply of low-emissions sources covered most of the increase in global electricity demand in 2024"—but not all of it. Natural gas and even coal had to step in to meet the shortfall.

Here’s the reality: the more renewables we add to the grid, the more clean, firm power we need to back them up. Without reliable baseload—like hydro, geothermal, nuclear, LTES or fusion—we’ll keep falling back on fossil fuels when the sun isn’t shining or the wind isn’t blowing.

To truly understand baseload's role in the energy mix, we must consider the key criteria that make one energy source better than another.

The most important factor is reliability—can the energy be accessed on demand? When we flip the light switch, we need immediate power. Without this reliability, energy loses all utility. The second crucial factor is cost—the cheaper the energy source, the better. Finally, we consider emissions. While low-emission or renewable sources are important, they offer little value if they're prohibitively expensive or unreliable. This was the challenge with renewables 10-20 years ago. This explains why, despite their high emissions, fossil fuels remain in widespread use—they provide stable, reliable, and low-cost energy. We need an energy source that is stable/accessible on-demand, low-cost and low emission.

Enter clean baseload.

Without a reliable source of 24/7 clean energy, we risk turning back to fossil fuels — undermining both our climate ambitions and energy security. Batteries are part of the answer, but today’s solutions are expensive and limited in duration. They can smooth out the day, not bridge a windless week.

To meet rising demand without retreating on emissions, we need to get serious about clean baseload — and fast.

Firm power sources bring balance to the grid. They reduce the risk of blackouts, help keep electricity prices stable, and support growing demand without sacrificing sustainability.

From an investment perspective, clean baseload power is a once-in-a-generation infrastructure opportunity. The global electricity market is worth over $2.5 trillion annually. Technologies that help decarbonize and stabilize the grid could unlock massive long-term value.

So, What Is Clean Baseload?

Clean baseload — or clean firm power (electricity) — refers to carbon-free energy that runs around the clock. Unlike wind or solar, it isn’t at the mercy of clouds or calm skies. It’s steady, weatherproof, and essential for the parts of our economy that can’t afford downtime: hospitals, factories, data centers, and the grid itself.

Three technologies stand out (the focus of this thesis):

- Geothermal taps deep underground heat to produce electricity or direct thermal energy — using techniques borrowed from oil and gas.

- Next-gen nuclear fission offers compact reactors with enhanced safety, smaller footprints, and smarter waste strategies.

- Fusion, long seen as a moonshot, is edging closer to reality — promising clean energy by replicating the same process that powers the sun.

These approaches aren’t new. But advances in materials, modeling, and manufacturing — plus a policy tailwind — are pulling them from the lab into the real world. What once felt like science fiction is now entering the realm of deployment.

Why Now?

Baseload power isn’t a new concept. But today, it’s newly investable.

Surging electricity demand, the pressure to decarbonize, and—most critically—breakthroughs in hard tech are converging to make clean, always-on energy both essential and viable. After decades of promise, we’ve entered the engineering era. For the first time in a generation, the timing is right for venture-scale opportunity.

Here’s what’s changed:

- The tech is breaking through. This is the key shift. Geothermal is moving from pilot to production, with companies like Fervo drilling commercial wells. Advanced nuclear projects are entering the licensing phase with real customers and regulators. Fusion has surpassed scientific breakeven in multiple configurations. What used to be theoretical is now being built—with timelines, budgets, and early traction.

- Demand is exploding. From transport and industry to heating and AI, more of the economy is electrifying. Data centers alone could double their energy use by 2026—and renewables can’t meet round-the-clock demand on their own.

- Reliability matters. Clean isn’t enough if it isn’t dependable. We need energy that shows up, rain or shine.

- Storage falls short. Batteries smooth hourly peaks, but cost-effective multi-day or seasonal storage is still out of reach. Long-duration storage is promising but not yet ready to carry the baseload burden.

- Energy security is back. Russia’s invasion of Ukraine reminded the world that energy dependency is a strategic vulnerability. Stable, domestic sources like geothermal and nuclear aren’t just climate tech—they’re national infrastructure.

The takeaway: we’re entering a window where clean baseload moves from theory to infrastructure. The next decade will determine whether we build it — or slide back to fossil fuels.

What Problem Are We Solving?

Wind and solar are essential — but they’re not always there when we need them. Clean firm power fills the gaps, keeping the lights on at night, in winter, and when the wind dies down.

Without it, we risk fragile grids, soaring costs, and a quiet return to fossil fuel backup.

Clean baseload solves for:

- Reliability: It keeps the grid stable when renewables fluctuate.

- Emissions: It cuts the need for gas or coal as fallback.

- Independence: It enables countries to build local, resilient power — not rely on imports.

- Cost: Clean baseload reduces the need to overbuild solar, wind, and batteries just to meet reliability targets. Instead of layering on excess capacity and storage to handle intermittency, firm power provides consistent supply—cutting redundancy, easing grid strain, and lowering total system costs.

What’s Working — and What’s Still Hard

Some breakthroughs are already in hand:

- Modular nuclear designs that are safer, easier to deploy and (some) cheaper.

- Real-world pilots of enhanced geothermal.

- Fusion experiments that have achieved net energy gain — a major scientific milestone.

But key hurdles remain:

- Regulatory inertia: Approving novel reactor designs takes years.

- Cost curves: Geothermal needs to drop in price to scale beyond niche applications.

- Fusion’s next leap: Moving from lab-scale success to grid-ready, continuous output.

In short: the physics works. The science is proven. What’s left is execution — engineering, permitting, and financing. And that’s exactly where startups and venture capital can have outsized impact.

Diving into Geothermal, Fission, and Fusion

Clean baseload energy typically revolves around several core technology categories: geothermal, hydropower, nuclear fission, fusion, next-generation biomass and underground long-term energy storage. Each follows its own timeline, carries a distinct risk profile, and unlocks different parts of the global energy map.

This thesis focuses on geothermal, advanced nuclear fission, and fusion. Let’s take them one by one.

Geothermal: Tapping the Heat Beneath Our Feet

Geothermal energy comes in three generations — each deeper, hotter, and more scalable than the last.

Generation 1: Conventional Hydrothermal

This is geothermal as most people know it: drill into natural underground reservoirs of hot water, inject cooler water, and use the resulting steam to drive a turbine. It’s been proven for decades in places like Iceland, Northern California, Turkey, and Japan. The downside? Less than 1% of the Earth’s surface has the right natural geology. Great where it works — but not a global solution.

Generation 2: Enhanced Geothermal Systems (EGS) & Closed-Loop

EGS engineers its own reservoirs by fracturing hot dry rock and injecting water to extract heat—geothermal borrowing tricks from oil & gas. Fervo Energy, a category leader, has raised over $400M and achieved key technical milestones, including successful horizontal drilling and fiber-optic monitoring. While traditionally seen as facing development—not science—risks, that narrative is shifting. Startups like Sage are pioneering approaches such as "pressured geothermal," which promise lower-cost, closed-loop systems with broader geographic potential. Many in the geothermal community now see these innovations as more scalable and near-term than superhot rock, keeping EGS firmly in the game for clean baseload energy.

Generation 3: Superhot Rock

The frontier play. Drill deeper and tap temperatures beyond 400°C. At that range, you unlock 2x more turbine efficiency and 3x more thermal energy — yielding 5–10x the energy output from a single well. In theory, superhot geothermal could work nearly anywhere. The main obstacle? Current drilling tools struggle to survive extreme heat, though isolated tests have already reached over 500°C. Startups like Quaise, GA Drilling, andHephae are developing next-gen plasma and millimeter-wave drills to crack this.

Why Geothermal Is Underrated

Geothermal may be the most overlooked clean firm power tech in the game. Unlike fusion or fission, it doesn’t require new science — just engineering gains, cost compression, and drilling scale.

Why it matters now:

- Proven technologies already in use (Gen 1) and in commercial deployment stages (Gen 2)

- Zero fuel costs, small land footprint, and 24/7 heat or power

- Oil & gas infrastructure — rigs, talent, supply chains — can be redeployed

- Superhot geothermal could make geothermal globally viable

- Commercial models span electricity, industrial heat, district heating, and co-located hydrogen or DAC

What’s still hard:

- Gen 1 is geographically limited

- Gen 2 is capital intensive and requires long-term reservoir stability

- Gen 3 is a tooling problem: a lot of components—electronics, batteries, and non-metallic parts—can’t survive the extreme conditions. We also need improved well completion methods, including casing and cementing, that can handle thermal cycling at 400°C and above.

- Cost per MWh is still too high in many markets

Why now:

- VC-timed milestones are emerging

- The oil & gas industry already drills ~70,000 wells per year — repurposing even a fraction of that could change everything

- Market share could jump from 0.015% of global energy to ~10% over two decades

- A natural transition path for oilfield service companies, if costs drop

Advanced Nuclear Fission: Compact Power, Familiar Physics

Fission has been around for decades, but new formats and fuels are reshaping what’s possible.

The Landscape

- Small Modular Reactors (SMRs): Factory-built, compact, and siting-flexible

- Gen IV Reactors: Use alternative fuels and coolants (e.g., molten salt, lead) for better safety and economics

- Microreactors: 1–20 MW systems for remote, industrial, or military uses

- Fuel innovation: Recycled nuclear waste, thorium, high-assay low-enriched uranium (HALEU)

Why Fission Still Has Legs

Advanced fission is credible — and, unlike fusion, it has a regulatory path, historical precedent, and engineering maturity.

Why it matters:

- Proven physics and decades of safety learnings

- SMRs offer faster build times, lower upfront costs, and passive safety

- Teams across Europe (e.g., Blykalla in Sweden, Seaborg in Denmark, Newcleo in France) are pushing forward on simplified, scalable designs

- Massive demand for clean, firm power — particularly from heavy industry and digital infrastructure

What’s hard:

- It’s not just a tech risk — it’s political, regulatory, and public opinion / acceptance

- SMR deployment requires multi-agency approval, siting agreements, off-take deals, and community buy-in

- Market entry involves a complex, multi-dimensional chessboard: tech, timing, trust, and supply chains

- Cost and time to market are the biggest barriers — SMRs under 500MW struggle to compete with coal on cost, and long build times mean interest rates can drive up large parts of total cost

Fission isn’t fast — but with the right team and market, it can be extremely durable.

Fusion: The Ultimate Long Bet

Fusion has long been the holy grail: fusing hydrogen isotopes at extreme temperatures—over 100 million °C—to release energy, like a star. The challenge is controlled confinement: keeping that superheated plasma stable long enough to generate power. It promises zero-carbon energy, no meltdown risk, and near-limitless fuel. For decades, the joke was that it was always 30 years away.

That timeline might finally be compressing.

Technology Approaches

- Magnetic confinement: Uses tokamaks or stellarators to trap hot plasma in magnetic fields

- Inertial confinement: Uses lasers or projectiles to compress and heat fuel pellets

- Alternative models: Z-pinch, mirror machines, or novel pulsed systems

- Enabling tech: High-temperature superconductors, plasma control algorithms, tritium breeding, neutron-tolerant materials

The physics of fusion is brutal: you need to hit the "triple product" — temperature (100 million+ °C), density, and confinement time. We've hit temperature and density. Time is the last frontier.

Can we trap this insanely hot, unstable stuff long enough for fusion to generate more energy than we put in?

Why Fusion Is (Finally) Getting Interesting

- Multiple startups (Commonwealth Fusion Systems, Helion, TAE) have hit major milestones — from net energy gain to gigagauss magnetic fields

- The ecosystem now includes both software and hardware innovation: advanced simulation tools, quantum models, diagnostics, and new materials that can withstand extreme conditions

- Spinout tech (e.g., superconducting magnets) has short-term market potential and can generate interim revenue

- Scientific proof of concept is likely this decade — commercial power could follow in the 2030s

Why It’s Still Tough

- Massive CapEx and long timelines: most fusion startups will require $1B+ before commercialization

- Proxima Fusion’s recent €130m Series A is based off of a proposed design, with their demonstration stellarator being scheduled to begin operations in 2031

- High engineering complexity, limited talent pool in plasma physics

- No obvious market pull yet: fusion lacks near-term offtake partners or regulatory blueprints

- First plants may be a decade away — even in a best-case scenario

Strategic View on Fusion

- It’s a go-big-or-go-home bet: extremely high risk, but fund-returner potential

- Milestone investing is key: clear technical checkpoints unlock value step by step

- Secondary markets and non-dilutive funding (e.g., ARPA-E, DoE) can help manage dilution

- Fund timeline fit is critical: investors need to align on 10+ year horizons and liquidity path expectations

- The long-term upside is massive, but the biggest risk may be obsolescence—if geothermal, fission, and renewables scale fast enough, the world may not need fusion to achieve abundant, cheap, clean power.

The Venture Lens: Timing, Risk, and Return

Clean baseload is not one market — it’s many distinct plays, each with its own blend of technical path, capital demands, and scaling timeline. For investors, the trick isn’t just backing the right science. It’s knowing which opportunity matches the kind of return profile venture capital is built for.

Global electricity demand is expected to double by 2045, driven by electrification of transport, heating, AI compute, and industrial growth. Electricity already accounts for over $3.5 trillion in annual global spend, and could exceed $7–10 trillion by 2040. Clean firm power — energy that’s available 24/7, regardless of weather — will be essential to meet this demand.

The opportunity is real. But not every bet is on the same clock — and not every exit looks the same.

Each of the three clean baseload technologies offers a different balance of scientific maturity, engineering risk, capital intensity, and exit timeline.

.png)

Not All Playing for the Same Prize

Let’s break it down across four dimensions: time to scale, market size, VC fit, and potential company outcomes.

Geothermal is moving fastest. Enhanced geothermal systems are already in commercial pilots, and superhot rock drilling is progressing rapidly. Deployment at scale is feasible within 5–10 years — well inside a typical fund’s holding period. The market could reach $200–500B by 2040, with venture-aligned opportunities across drilling tech, project development, and energy-as-a-service models. It’s modular, capital-efficient, and ripe for $1–5B outcomes.

Advanced fission is slower, with timelines of 7–12 years (albeit with some companies already planning to build in 2027-28) depending on licensing and siting, but the market is enormous. The TAM for clean industrial power and grid baseload is estimated at $500B–1T.

Fusion has the longest timeline — but also potentially the biggest prize. First grid-connected power plants are unlikely before the 2030s, but the scientific breakthroughs are real. Commonwealth Fusion Systems, Helion, and others have raised hundreds of millions — with milestone-driven valuation jumps. The total addressable market could exceed $1T if fusion lives up to its promise. And even if it takes longer, spinout technologies like superconductors and plasma control systems can generate near-term revenue.

So, What’s the Take?

- Geothermal is closest to scale and most aligned with typical VC timelines

- Fission has bigger upside per unit but requires patience, regulation, and long sales cycles.

- Fusion is potentially the most transformative bet — and the least liquid in the near term.

All three could produce generational companies. But they aren’t playing the same game — or on the same timeline.

.png)

.png)

.png)

We Believe (“Our Hypothesis in the Longer-Term”)

At byFounders, we believe the energy transition won’t be completed without abundant, affordable, and clean baseload power. Renewables will dominate the supply mix, but without firm power, they won’t be enough to deliver net-zero at scale. Here’s how we expect the market to evolve:

Hypothesis 1: Clean firm power is the keystone of a decarbonized grid

Without geothermal, advanced fission, or fusion, grids will remain dependent on fossil peaker plants. The cost and carbon savings from high-renewables grids plateau unless clean baseload fills the reliability gap. We believe these technologies will define the backbone of the energy transition.

Hypothesis 2: Geothermal leads near-term deployment, fusion dominates long-term upside

Advanced geothermal will reach meaningful commercial scale in the next 5–7 years, particularly through partnerships with oil & gas and heating utilities. Fusion has the potential to reshape energy economics entirely—but likely on a 10–20 year horizon. Fission, by contrast, is already a mature and bankable technology. While deployment takes time, it’s improving steadily and remains the most proven path to energy sovereignty and reliable power in remote or energy-poor regions.

Hypothesis 3: Hyperscaler demand will accelerate first deployments, but rising global demand and energy sovereignty are the enduring drivers

Hyperscalers provide early momentum by acting as strategic, patient offtakers—signing long-term PPAs to meet 24/7 clean energy mandates. For them, energy is mission-critical but still a small fraction of AI infrastructure costs, making them willing to pay a premium for clean, firm power. But the larger force is global demand: electricity use is set to double over the next 25 years, driven by rising living standards across Southeast Asia, Africa, and Latin America. As billions gain access to EVs, air conditioning, and electric heating, nations will prioritize sovereign, stable, clean baseload—turning technologies like advanced nuclear, geothermal and fusion into critical infrastructure.

byFounders Investment Focus

Our investment strategy in clean baseload energy is grounded in deeptech principles but tuned for commercial pragmatism. We’re targeting technologies that combine transformative potential with tangible milestones over a 5–10 year horizon.

We’re not just backing technologies — we’re backing enabling infrastructure, market catalysts, and talent that can move industrial-scale energy forward with venture-level speed. Our goal is to identify segments that allow staged de-risking, cross-vertical relevance, and IP defensibility — all while operating in capital-intensive environments where execution is often the differentiator.

What We Look For

- LCOE competitive with coal: Self-explanatory—needs to outcompete fossil fuels on all parameters. That means achieving cost parity with coal without relying on carbon pricing or subsidies (that goes both ways). Coal is incredibly cheap if you exclude its environmental and health externalities, so true competitiveness means matching it on pure market terms.

- Stepwise de-risking: Clean baseload companies are often multi-stage. We look for ventures that divide their risk into addressable phases — for instance, science validation, subscale prototyping, first-of-a-kind deployment, and commercial rollout. Each stage should unlock external validation, follow-on capital, and strategic partnerships.

- Enabling technologies: Rather than betting only on headline generation companies, we focus on the critical, underappreciated enablers — for instance, companies making precision-drilled geothermal wells feasible through AI-guided plasma drilling, or startups producing reactor-compatible materials that withstand 1000°C conditions. These companies generate value independently and improve the economics of the entire sector.

- Modularity and platform potential: Technologies that are modular can reach scale faster, enter markets flexibly, and avoid the “all-or-nothing” dynamic of megaprojects.

- Capital efficiency: While we understand these ventures won’t be capital-light, we believe that winning teams can raise and deploy early capital with surgical efficiency. We assess not just how much capital is needed, but what each tranche unlocks.

- Founder-market fit: In baseload energy, teams must span disciplines: nuclear physicists, thermal engineers, industrial project managers, and regulatory experts. The strongest teams can navigate hardware risk, regulatory inertia, and grid politics while keeping a clear, investor-aligned path to commercial traction.

Our Focus Areas Today

As we look across the clean firm energy landscape, we’re particularly focused on startups and technical wedges that combine large long-term potential with meaningful intermediate milestones. Here are five themes we’re especially excited about:

Superhot Geothermal Drilling Tech

The frontier of geothermal lies in ultra-deep, ultra-hot wells — where rock temperatures exceed 400°C and energy density soars. Tools like plasma drills (GA Drilling) or millimeter-wave beam systems (Quaise) are essential to accessing these depths. For VCs, the pitch is clear: these companies are selling the “picks and shovels” of a gold rush. If the tech works, it enables geothermal anywhere — even in geologies previously deemed non-viable. If geothermal can grow from its current 0.015% to even 10% of global energy, the enablers of this shift stand to see explosive upside. The upside is leveraged by the fact that oil & gas rigs, talent, and supply chains are repurposable, making scalability more about economics than physics.

Advanced Nuclear Fuel & Waste Solutions

The success of advanced fission hinges not just on reactor design but also on fuel cycles and waste handling. This includes ventures working on high-assay low-enriched uranium (HALEU), molten salt fuels, or fast reactors that consume existing spent fuel. The opportunity here is twofold: reduce the front-end constraint of enriched fuel access, and monetize back-end waste streams. These technologies often have lower CapEx than full reactors and can serve early adjacent markets — like medical isotopes, space applications, or national lab contracts. From a VC lens, they are the critical “middleware” of the nuclear stack: not as capital intensive as full-stack players, but deeply essential to unlock long-term value.

Modular Geothermal Heat & Power Platforms

Modular systems — particularly closed-loop or shallow-well geothermal — offer a rare sweet spot for VC: they’re deployable at the building or district scale, can generate either heat or power, and can be rolled out incrementally. Heat is often the overlooked half of global energy demand. Startups targeting heat-for-industry or geothermal-powered data centers have clear market pull and short sales cycles. Additionally, modular systems can often plug into existing geothermal heat loops in places like Germany or the Nordics, making regulatory paths and infrastructure integration easier.

Fusion with Potential for Spinouts with Intermediate Markets

The long arc of fusion will take decades to reach grid parity (price competitive) — but along the way, many enabling technologies can commercialize far earlier. Superconducting magnets, precision plasma diagnostics, fast-switch power electronics, or neutron generators have immediate applications in medical imaging, industrial inspection, or even space propulsion. These companies often spin out of major fusion ventures or labs and bring with them IP, credibility, and deeptech talent. For VCs, the attraction lies in their dual-track potential: near-term revenue in known markets, with an eventual optionality on becoming part of the fusion stack.

AI for Autonomy, Safety & Simulation

As clean firm power assets become more complex and operate in harsher conditions, AI is emerging as a critical layer. Machine learning can optimize real-time plasma confinement in fusion, predict subsurface anomalies in geothermal drilling, or simulate failure modes in SMRs. The software layer in hardtech ventures is often underpriced — yet it can improve margins, shorten design cycles, and unlock autonomous operation. Startups in this space can follow a SaaS-like trajectory (via licensing or enterprise contracts) while being deeply embedded in physical infrastructure.

We’re Open to What’s Next

While these focus areas reflect our current conviction zones, they’re far from exhaustive. We know that many of the most transformative companies won’t fit neatly into today’s categories — and we’re excited by that.

If you’re building something that:

- Pushes the boundaries of how we generate, store, or distribute clean firm power

- Brings a fresh approach to energy hardware, software, or financing

- Unlocks previously uneconomical energy resources through technology

- Or rethinks infrastructure from the bottom up for a net-zero world…

…we want to hear from you.

Related

Sign up to our newsletter.

Follow us