VC 101 - Cultivating a Venture Mindset

Forget everything you thought you knew.

This post was originally published on martinkrag.substack.com. Want to read more of Martin's thinking? Subscribe to his Substack here!

For the past few years, as I’ve been onboarding our new hires at byFounders, it has become clear to me that one of the most important indicators of success is whether and how quickly new recruits can calibrate their mindset and tune into venture frequency.

Coming from startups, consulting, or university, joining a venture capital fund with little or no prior VC experience, can be daunting, as the learning curve is steep and may even require you to unlearn a bunch of skills and practices that you’ve cultivated over time. It doesn’t help that the venture capital industry is somewhat of a blackbox and that the perceived and actual reality of the job might not align.

Over the years, I’ve developed various materials to help cultivate that venture mindset for people joining our ranks unfamiliar with the intricacies of the VC industry. We’re sharing some of it here. Hopefully it’s helpful if you’re looking to start or are just getting started in VC.

One caveat to keep in mind: at byFounders we invest at the earliest stages and VC is likely more an art than a science. What works for us might not work for others and later stage firms will undoubtedly look at things different than we do.

Alright, let’s jump in – here’s today’s menu:

- Venture Capital is a game of big swings, home-runs, and strike-outs

- Investing is simple (but not easy)

- The feedback loops are long and the input-output causality is weak

1. Venture Capital is a game of big swings, home-runs, and strike-outs

The first thing to understand is that VC is about an unbounded upside and limited downside. You can only lose 1x of your investment, as they say, while the best investments can return multiples in the 100s or even 1000s.

Contrary to the thinking in PE, hedge funds, or among public investors, protecting the downside should not matter as much to VCs — as long as they are able to find and fund those companies with that nearly uncapped upside.

Second, a common misconception is that Venture Capital = Investing in Startups. The conditions that make a company a potential 100x or 1000x investment return are so restrictive in scope that it only applies to a narrow subset of all startups out there. As such, venture capital is not appropriate for all startups and all startups should not seek venture capital.

Instead, I like to think of venture capital as:

a very specific instrument used to fund companies that are capable of explosive value creation over compressed periods of time, by building and launching products in stages, unlocking new pools of capital as the opportunity is gradually de-risked.

As such, the job to be done as a VC is not merely to “invest in startups”, rather it is to find and fund outliers and improve the founders' odds of building a truly generational company.

Let us look at the math driving home this point.

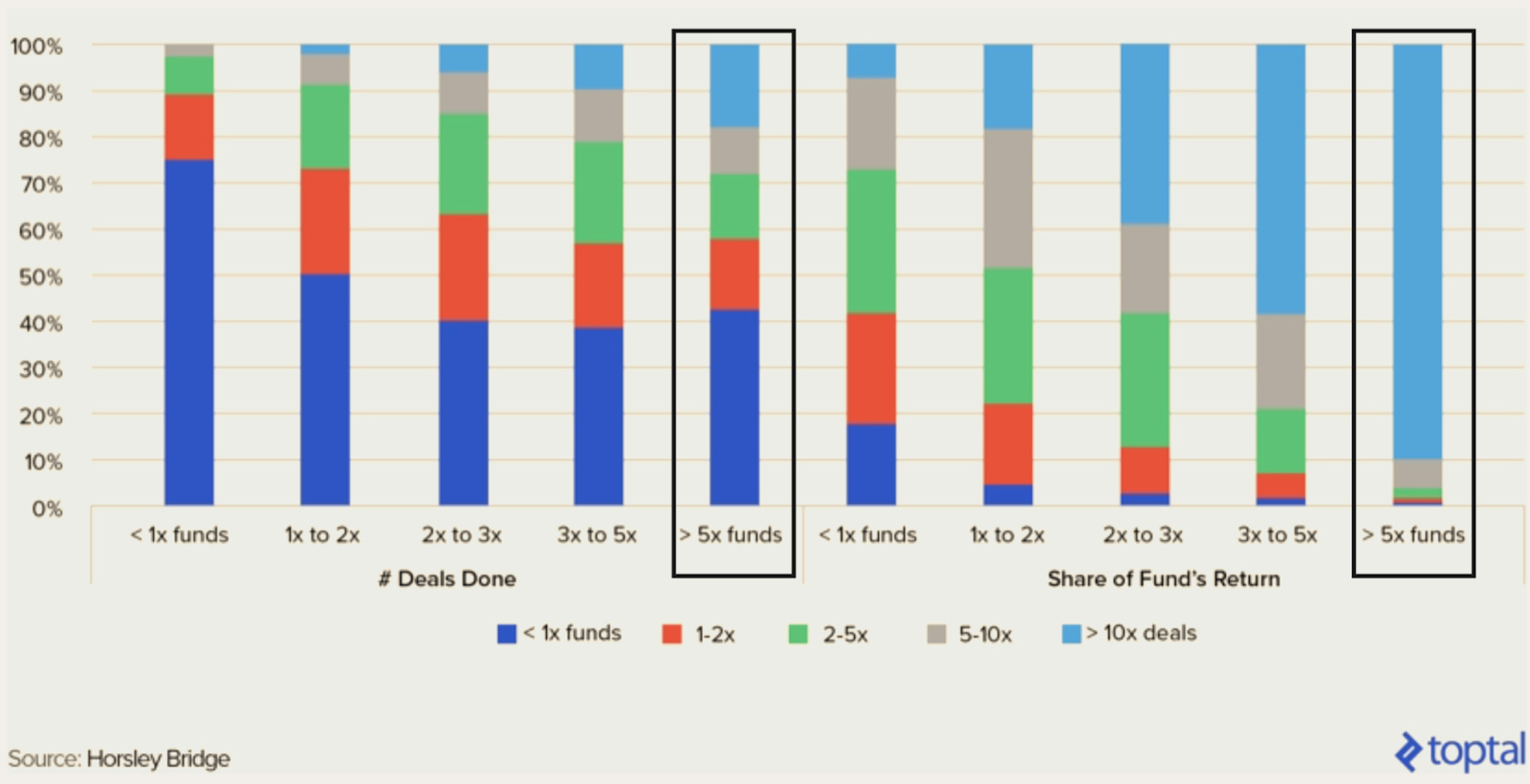

It is close to a mathematical fact that startup investment returns follow a power law distribution where the majority of investments goes to zero and the returns come from a few.

For funds returning more than 5x (which is very good), less than 20% of the investments produced (the light blue bar highlighted centrally) roughly 90% of the funds’ returns (light blue bar highlighted furthest to the right)

In other words, VC returns are driven by outlier companies. The best investment in a successful fund equals or outperforms the entire rest of the fund combined.

Swinging for the fences trying to hit a home-run is going to result in a lot of strikeouts. This is the name of the game. Interestingly, the great funds (>5x returns on a fund level) have more (and higher) losses than the good funds (3x) – but naturally not as many as the bad funds.

To sum everything above up in an Altman tweet:

2. Investing is simple (but not easy)

VCs are by nature capital allocators while founders do the heavy lifting of building enduring and generational companies.

At the core, investing is very simple, at least if you subscribe to few of the truisms in the industry.

The consequence of the power law nature of the industry is, as Tyler Durden Peter Thiel puts it:

"There are two rules in Venture Capital. First, only invest in companies that have the potential to return the value of the entire fund. This leads to rule number two: because rule number one is so restrictive, there can’t be any other rules"

Simple, right? But hardly easy to gauge the true potential of a company at the earliest stages of investing

Or how about this simple rule:

Again – extremely simple on the surface level and something I believe to be true. But identifying what outstanding is and finding, selecting, and winning the opportunity to invest in such outstanding founders – repeatedly – is definitely not an easy feat. Further, history is filled with “massive opportunities” that have turned out to be the exact opposite, while a lot of VCs have been incredibly wrong in declining companies because of the total addressable market presumably not being large enough.

At its core, I see early stage (pre-seed and seed) investing as a people + insights business. Backing the right team is undoubtedly a necessary condition for success but insights are what end up moving the needle. The founder’s insight about the problem, an insight about the customer segment, or a technological insight, as well as the investor’s insight about the market, the timing, the competitors, and the founding team.

3. The feedback loops are long and the input-output causality is weak

Another difficult thing to square for many people new to venture capital is the length of the feedback loops and the causal uncertainty between inputs and outputs. Basically, you won’t know if you’re any good at investing until 5-10 years later – and even then you might just have gotten lucky and/or have had very little to do with the outcome.

- Year 1: “Am I not good if a great VC invests in the later rounds of my portfolio?” Too soon to tell – the next investor might be as oblivious as you are.

- Year 2: “Another uptick, the company is now a unicorn! Surely, I must know what I’m doing now?” A lot of factors contribute to paper markups and you still can’t eat IRR.

- Year 5: “I got an exit! – small but returned my investment 5x”. If you invest at the early stages from a mid-sized fund, 5x on an early ticket hardly makes a dent for the overall return profile of the fund (see above).

- Year 8: “Boom! I returned the fund on just one company’s exit!”. Getting there, now prove you can do it all over again – once is chance, twice is coincidence, third time's a pattern, as they say.

VCs are quick to take (part of) the credit for the successes while they obviously had very little to do with the failures. The greatest VCs know that regardless of what part they have played in a great outcome, they are never better than their latest investment and hence stay humble and hungry even after several successes.

Joining a VC as a former founder or operator can be particularly challenging, as you quickly need to adjust the input-to-output loop from days and weeks (build and ship a feature, get feedback) to months (making an investment) and years (knowing if it has any potential to be a good investment).

You can be short-term right but long-term wrong and vice versa – and you won’t know for a while.

Additionally, the outlier nature of venture means that your whole career can (and likely will) come down to getting one single decision right.

Make sure you go into VC for the right reasons. If you want to build, ship, and tinker with the latest technology, you’ll have your needs better met in a startup. If you’re endlessly curious, great at context switching, enjoy breadth over depth, and are comfortable with being wrong but confident that you might be right – well, then venture capital might be just the right place for you.

Curious to learn more and about cultivating a venture mindset and developing frameworks for your decision-making? Subscribe to catch the next post from me:

VC 201 - The VC Success Equation: Three necessary (but not sufficient) conditions to succeed in VC

Related

.jpg)

Sign up to our newsletter.

Follow us